When you buy a home or renew your mortgage, your lender will likely offer you mortgage protection insurance. It sounds like a convenient way to protect your family and your biggest asset. However, before you sign on the dotted line, it is crucial to understand exactly what you are buying—and what you might be giving up.

For most Canadians, personal term life insurance offers superior flexibility, reliability, and financial security compared to lender-provided mortgage insurance. Let us break down the key differences between the two so you can make the best decision for your family’s future.

What is Mortgage Protection Insurance?

Mortgage protection insurance (often simply called mortgage life insurance) is a policy you purchase through your mortgage lender or broker. Its sole purpose is to pay off or pay down your outstanding mortgage balance if you pass away.

While it provides a basic level of protection, it comes with several significant limitations that many homeowners do not realize until it is too late.

What is Personal Term Life Insurance?

Personal term life insurance is a policy you purchase independently through an insurance advisor or broker. It provides a guaranteed, tax-free lump sum payment to your chosen beneficiaries if you pass away during the specified term (such as 10, 20, or 30 years).

Unlike mortgage insurance, term life insurance is entirely separate from your mortgage and your lender, giving you complete control over your coverage.

Key Differences: How They Stack Up

When comparing the two options, several critical differences emerge regarding who gets the money, how much coverage you actually have, and when the underwriting happens.

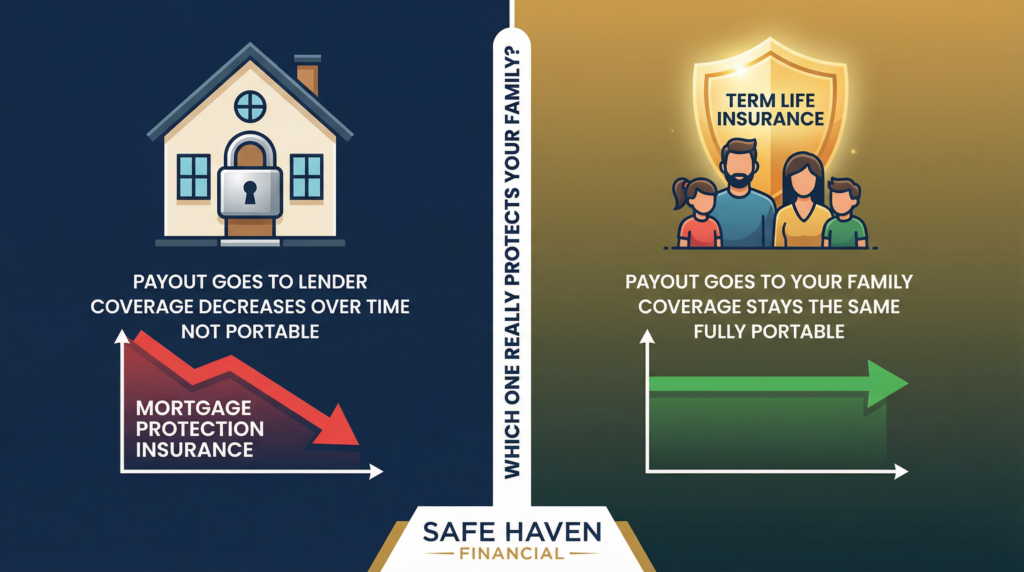

1. Who Receives the Payout?

Mortgage Insurance: The payout goes directly to your lender, not your family. The money can only be used to pay off the mortgage balance.

Life Insurance: The payout goes directly to your chosen beneficiaries (such as your spouse or children). They receive a tax-free lump sum that they can use for anything—paying off the mortgage, covering daily living expenses, funding a child’s education, or investing for the future.

2. Does the Coverage Amount Change?

Mortgage Insurance: Your coverage decreases as your mortgage balance shrinks. Because the policy only covers the outstanding mortgage amount, the value of your insurance drops with every mortgage payment you make. However, your premium payments typically remain exactly the same.

Life Insurance: Your coverage remains consistent. If you purchase a $500,000 term life policy, your family will receive exactly $500,000 if you pass away during the term, regardless of how much you owe on your mortgage.

3. Is the Policy Portable?

Mortgage Insurance: The policy is tied to your specific lender and mortgage. If you sell your home, switch lenders to get a better interest rate, or refinance, your coverage ends. You will have to reapply for new insurance at your older age, which will likely be more expensive.

Life Insurance: The policy is fully portable. It stays with you no matter where you live, which bank holds your mortgage, or how many times you refinance. You own the policy, not the bank.

4. When Does Underwriting Happen?

This is perhaps the most critical difference between the two types of insurance.

Mortgage Insurance: Underwriting typically happens at the time of claim. When you apply, you usually only answer a few basic health questions. However, if you pass away, the insurer will investigate your medical history to determine if you actually qualified for the coverage. This process, known as post-claim underwriting, leads to a higher chance of claim denial when your family needs the money most.

Life Insurance: Underwriting happens upfront. When you apply, the insurer fully assesses your health and medical history before issuing the policy. Once you are approved, you have absolute certainty and peace of mind knowing that the coverage is guaranteed to pay out to your loved ones.

5. How Do the Costs Compare?

Mortgage Insurance: Despite offering decreasing coverage, mortgage insurance is typically more expensive than term life insurance for the same initial coverage amount. You are essentially paying a level premium for a shrinking benefit.

Life Insurance: Term life insurance is generally much more cost-effective, especially for younger and healthier individuals. You pay a set premium for a guaranteed, level amount of coverage that provides significantly more value over time.

Summary Comparison

| Feature | Mortgage Insurance | Term Life Insurance |

|---|---|---|

| Beneficiary | The mortgage lender | Your family (you choose) |

| Coverage Amount | Decreases as mortgage is paid down | Stays exactly the same |

| Portability | Tied to your lender; ends if you switch | Fully portable; stays with you |

| Underwriting | At claim time (higher risk of denial) | Upfront (guaranteed payout) |

| Cost Value | Typically more expensive for less coverage | More cost-effective, level coverage |

Which is Right for You?

While mortgage protection insurance might seem convenient because you can sign up for it at the bank while finalizing your mortgage, it rarely offers the best value or protection for your family.

Personal term life insurance empowers your family to make the best financial decisions in any situation. It provides a guaranteed safety net that they control, not the bank. If the worst happens, your loved ones can choose whether to pay off the mortgage entirely, continue making monthly payments while investing the rest, or use the funds to maintain their standard of living.

Do not leave your family’s financial security to chance with post-claim underwriting and decreasing coverage. Protect what truly matters with a policy you own and control.

Ready to secure the right protection for your family? Contact Safe Haven Financial today to compare term life insurance quotes and find a policy that fits your needs and budget.